![]() English

English ![]() हिन्दी

हिन्दी ![]() Indonesia

Indonesia ![]() Português

Português ![]() Tiếng Việt

Tiếng Việt ![]() العربية

العربية ![]() ไทย

ไทย

Markets were under pressure due to the unscheduled Fed meeting on 14.02. Participants were anticipating that after such terrible inflation data the FOMC would take urgent measures and raise the rate. But… nothing terrible happened.

Weekly Trends

- Microsoft 3.76%. Trading down with $100 and a X20 multiplier, you could have easily made $75.2.

- NZD/USD 0.35%.Trading up with $100 and a X500 multiplier, you could have easily made $175.

- BTC 4.7%. Trading down with $100 and a X10 multiplier, you could have easily made $47.

Currency Markets

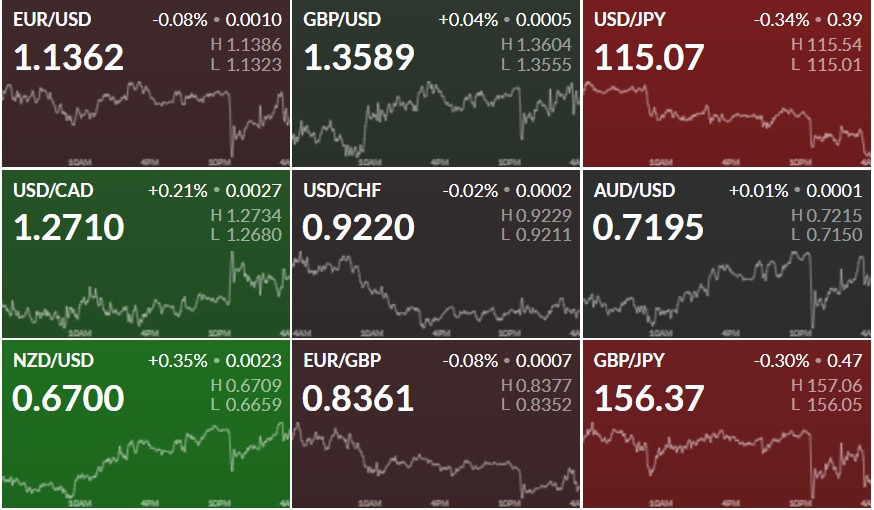

There were no significant changes on the currency market during the week. On 14.02, there was an unscheduled meeting of the US Federal Open Market Committee (FOMC), but no decisions regarding an interest rate hike were made. In response, EUR/USD, which at the beginning of the week was in a downtrend, leveled out and remained almost unchanged. The DXY index stayed above 95.7, but we see no growth yet.

Register Olymp Trade & Get Free $10,000 Get $10,000 free for newbies

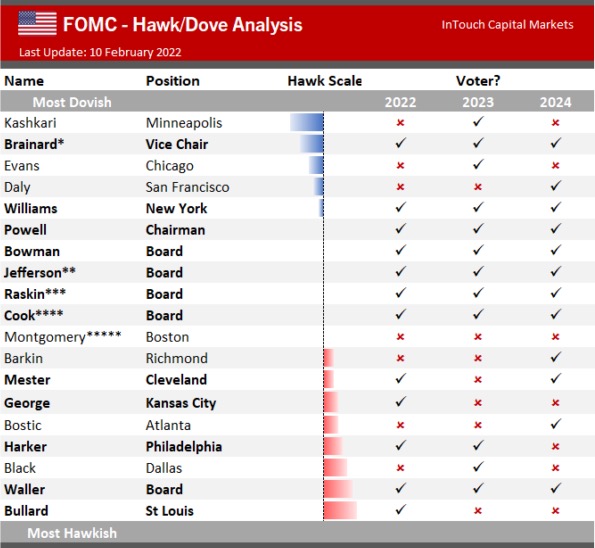

The next scheduled FOMC meeting is 16.03.2022. Right now analysts are almost 100% sure that the rate will be raised by 25-50 bp to the range of 0.25-0.5%. Currently, the majority of voting FOMC members are in favor of a rate hike (hawks).

Even Lael Brainard, who is the only remaining supporter of soft monetary policy, made a statement this week that “the Fed’s rate is the main tool for fighting inflation”

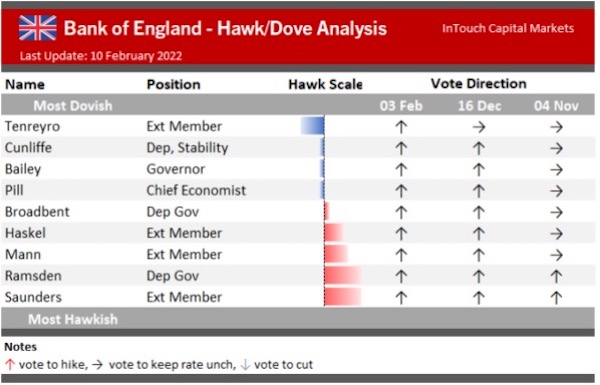

The situation with the Bank of England, which has already launched a system to absorb excess liquidity, looks no less interesting. The majority of voting members of the BoE are also in favor of raising the interest rate.

This means that there is a high probability that the bank’s policy will remain tough. For the markets, it means the following:

- GBP might continue to rise against other currencies. Cross rates such as GBP/CHF and GBP/JPY are especially worth considering.

- The British FTSE could turn around and start to decline.

Register Olymp Trade & Get Free $10,000 Get $10,000 free for newbies

Stock Markets

The U.S. stock market is mostly in the “red” this week. Technology, Communication Services, and Consumer Cyclical sectors are the worst performing stocks.

The worst day for the indices was Valentine’s Day on 14.02. The markets were Risk-off due to the upcoming, unscheduled, FOMC meeting. The Dow Jones nearly broke the 34400 level down, the Nasdaq100 fell below the level of 14400, and the S&P 500 tested 4400. Later, when it became clear that there would be no sharp moves on the interest rate, bulls managed to recapture the initiative and the indices moved slightly from their key levels.

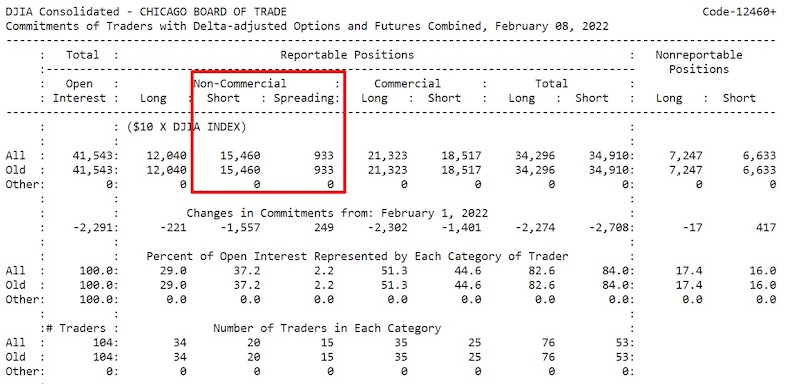

According to the CFTC report for the last week, the situation has not changed much. The number of short positions of large market participants still exceeds the number of long positions.

Last week, we looked at Amazon stock. The bulls, however, failed to overcome the resistance level of $3,200-3,300, which means that there is still a chance of a further decline.

The U.S. market will be closed on Monday due to “President’s Day”.

Commodity Markets

Brent crude oil updated its new maximum to $95.42 per barrel, which corresponds to the Fibo level of 1.5 of the current trend. We haven’t seen such prices in more than 7 years. Nevertheless, the trend line has been broken locally, which technically was expected because the price has been in an overbought condition for a long time. Local support for Brent is at the level of $90 and the Fibo level of 1.236.

The fundamental reason for the correction may be the progress in the US- Iranian nuclear negotiations. It has not yet been officially announced, but the negotiators claim they are “closer than ever to a deal”. If the parties reach an agreement, oil sanctions will be lifted from Iran. Iran is one of OPEC’s largest suppliers, and it has the ability to increase capacity significantly.

This could potentially create a surplus of nearly 1 million barrels per day. In this case, the price of Brent could drop by $10 or more. However, OPEC+ is not yet able to fulfill its own plans to increase production and Iran would greatly help solve this problem. The most important question today is how quickly the country will be able to reactivate its full production capacity, which hasn’t been used for some time. This will be the key unknown in the equation.

From a technical point of view, last week was more than successful for Gold. Here are some of the reasons:

- The key resistance level at $1876 was broken.

- The price is close to $1900 per troy ounce, opening the way to the next psychological level of $2000.

- The downtrend line, in which gold has been trading since August 2020, was finally broken.

The sharp increase in price led the asset to the overbought area on the RSI for the first time since November of last year. Therefore, it is quite possible to expect a local correction after the current spike.

The rise in gold reflects the fleeing of investors from risky assets to safe haven assets. The stock market continues to decline, U.S. government bond yields are also dropping, and inflation is breaking records. Additionally, there are geo-political issues such as escalations and potential conflict between Russia and Ukraine as well as the resolution of the Iranian nuclear program. If the U.S. and Iran come to an agreement, it would destabilize the situation with forces in the region.

Cryptocurrency Markets

Bitcoin has been consolidating in the range of $41,000-46,000 for the past 2 weeks. An exit from this range will determine the mid-term market sentiment. If the resistance level of $46,000 is broken, then we can talk about the start of an upward correction. If $41,000 support fails to hold, then the mid-term bearish trend will continue. In that case, the daily MACD and several other indicators will show downside signals. This may lead to a new wave of sales and a return to the global support area of $30,000-34,000. However, by all metrics, the market is in a neutral position.

Register Olymp Trade & Get Free $10,000 Get $10,000 free for newbies

The upcoming month promises to be interesting. JPMorgan strategist David Kelly thinks cryptocurrency investors could suffer serious losses because of the Fed’s interest rate hike. This will end the era of “crazy speculation”. It was revealed in the FOMC meeting minutes from January 25-26 that the regulator notes increasing risks to financial stability due to the rapid growth of crypto assets and DeFi platforms.

The capitalization of the crypto market returned to $2T. Daily trading rose to $77.8B.

The Fear and Greed Index remains in the Neutral position displayed at 52 points. Retail traders are also evenly distributed with sellers strongly dominating on FTX Kraken and buyers on Bitfinex. The BTC Dominance Index remains around 40%.

JPMorgan joins metaverse. The bank has opened a lounge in a Decentraland project. The location is called Onyx, after the bank’s blockchain platform. It features a report from JPMorgan on business opportunities in virtual metaverses.

Central Bank of Russia: CBDC – yes, cryptocurrencies – no. The Central Bank of Russia will begin stage 2 testing of the digital ruble in the fall of 2022. Transactions payments for goods, services, and government payments will be tested. Meanwhile, Russia’s Ministry of Finance has prepared a bill to regulate the crypto industry, despite the regulator’s point of view.

Register Olymp Trade & Get Free $10,000 Get $10,000 free for newbies

Cryptocurrency business is expanding. The amount of mergers and acquisitions in the cryptocurrency sector exceeded $55B in 2021. In 2020, it was only $1.1B.

Conclusions

- The currency market is almost unchanged this week. It’s worth paying attention to the British currency, which may start to rise with the hawkish mood of the Bank of England.

- Indices are down. The bulls managed to bounce back from Friday’s big drop, but it’s too early to relax. The Open Market Committee is due to meet in mid-March. The probability of a rate hike is nearly 100%.

- Oil is renewing its highs and approaching $100. Gold has broken through the global trend line and is rapidly rising towards $2,000.

- The cryptocurrency market is in a neutral position according to the main metrics.

![]() English

English ![]() हिन्दी

हिन्दी ![]() Indonesia

Indonesia ![]() Português

Português ![]() Tiếng Việt

Tiếng Việt ![]() العربية

العربية ![]() ไทย

ไทย

")

General Risk Notification: Transactions offered by Olymp Trade can be executed only by fully competent adults. Transactions with financial instruments offered on Olymp Trade involve substantial risk and trading may be very risky. If you make Transactions with the financial instruments offered on Olymp Trade, you might incur substantial losses or even lose everything in your Account. Before you decide to start Transactions with the financial instruments offered on Olymp Trade, you must review the Service Agreement and Risk Disclosure Information. Olymp Trade is operated by Saledo Global LLC; Registration number: 227 LLC 2019; Registered Office Address: First Floor, First St. Vincent Bank Ltd Building, P. O Box 1574, James Street, Kingstown, St. Vincent & the Grenadines.

General Risk Notification: Transactions offered by Olymp Trade can be executed only by fully competent adults. Transactions with financial instruments offered on Olymp Trade involve substantial risk and trading may be very risky. If you make Transactions with the financial instruments offered on Olymp Trade, you might incur substantial losses or even lose everything in your Account. Before you decide to start Transactions with the financial instruments offered on Olymp Trade, you must review the Service Agreement and Risk Disclosure Information. Olymp Trade is operated by Saledo Global LLC; Registration number: 227 LLC 2019; Registered Office Address: First Floor, First St. Vincent Bank Ltd Building, P. O Box 1574, James Street, Kingstown, St. Vincent & the Grenadines.